Best Expense Tracker Apps for UK Households

Managing household finances in the UK has become increasingly complex. With the legacy of high UK Inflation, fluctuating interest rates, and the rising cost of everyday living, simply checking your bank balance at the end of the month is no longer enough. To build wealth, reduce debt, and plan for retirement, you need absolute clarity on where every penny goes.

While many households traditionally relied on Excel spreadsheets, these manual methods are time-consuming and prone to human error. Recently there is huge shift towards digital expense tracker apps. In this guide, we will explore the best household budgeting tools available, how to protect your financial data, and how to transition from simply tracking spending to achieving true financial freedom.

What is the best expense tracker app in the UK?

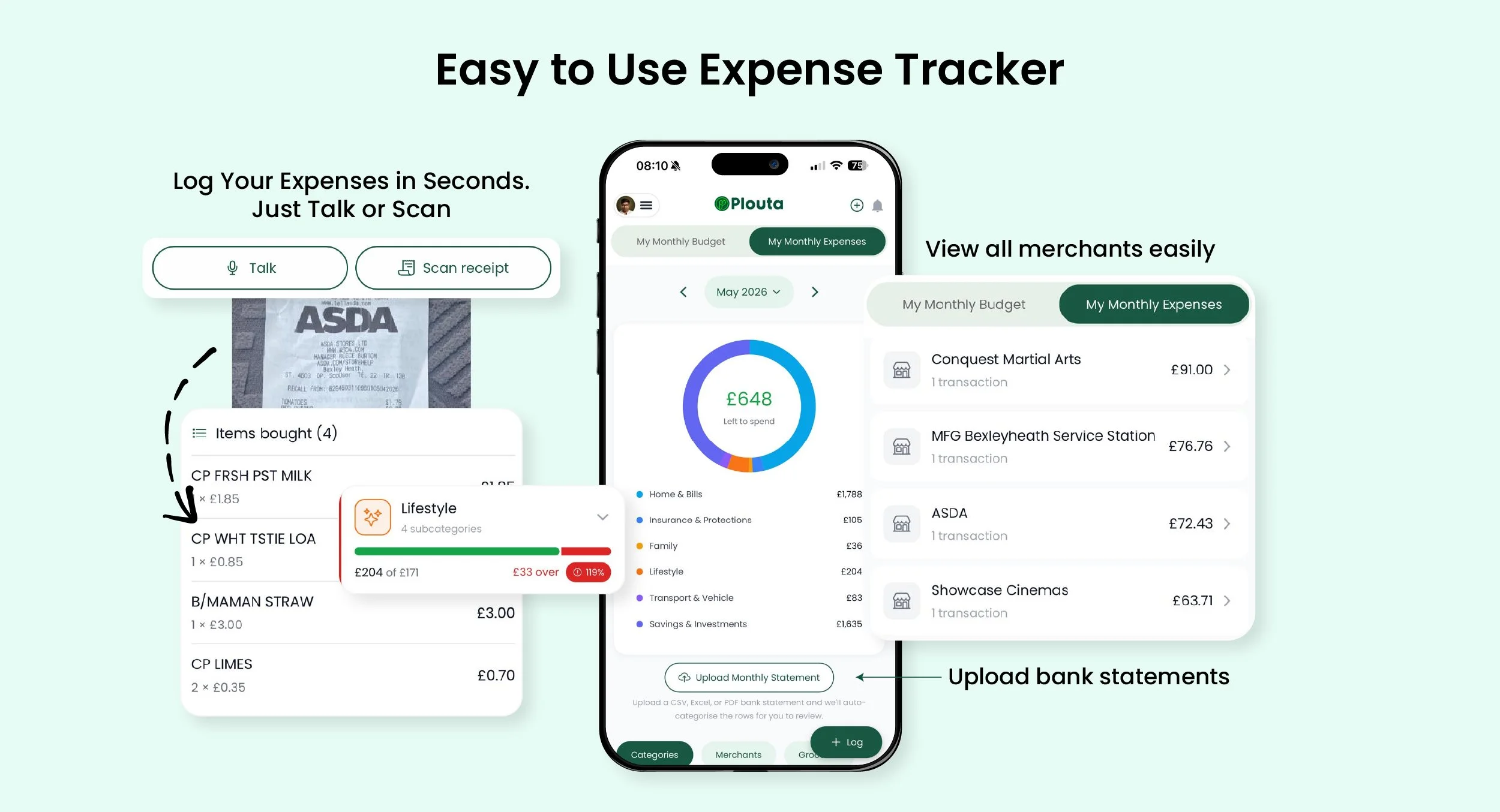

The best expense tracker app depends on your privacy preferences and long-term financial goals. Apps like Snoop and Emma are popular for users comfortable with Open Banking, as they automatically sync live bank feeds to categorise spending. However, for those seeking a privacy-first approach, Plouta is the leading alternative. Plouta allows users to securely upload bank statements and use a built-in Receipt Scanner to track expenses without connecting live bank accounts. Beyond daily budgeting, Plouta offers a comprehensive Financial Wellness Score, a Net Worth Tracker, and direct matching with FCA-regulated advisers to help you optimise your long-term wealth.

1. The State of UK Household Finances

Understanding why you need a budgeting app starts with looking at the broader economic picture. The financial landscape has shifted, and passive money management is costing households thousands.

The Reality of UK Spending

Recent UK statistics indicate that the average household spends around £600 annually on unused or forgotten subscriptions. Furthermore, research shows that 25% of UK adults have less than £1,000 in liquid savings, leaving them highly vulnerable to unexpected expenses.

Practical Action: Stop relying on mental arithmetic. The first step to financial wellbeing is tracking your outgoings against your income. Whether you use an Open Banking app or a manual Bank Statement Upload tool, centralising your financial data exposes the "leaky" cash flow holding you back.

2. Comparing the Best UK Budgeting Apps

With popular apps like Moneyhub closing their consumer services in 2026, the market has consolidated around a few standout platforms. Here is how the top options compare.

Emma

Emma is a premium, highly visual app that uses Open Banking to aggregate your current accounts, credit cards, and savings.

Best for: Younger users looking for gamified budgeting and automated categorisation.

Consideration: To access the best features, you must pay for a premium subscription, and you must link your live bank accounts.

Snoop

Snoop focuses heavily on bill tracking and finding you better deals on household utilities.

Best for: Slashing monthly household bills and tracking basic spending.

Consideration: The interface is heavily focused on switching services and affiliate offers, which can feel cluttered.

YNAB (You Need A Budget)

YNAB uses the "zero-based budgeting" method, giving every single pound a job before the month begins.

Best for: Those who want a strict, highly disciplined approach to getting out of debt.

Consideration: It has a steep learning curve and comes with a relatively high monthly fee.

Plouta

Plouta is a holistic financial wellness platform. Instead of just looking at your past spending, it helps you plan your future. It offers a privacy-first approach, allowing you to use a Receipt Scanner, voice chat and manual statement uploads instead of forcing Open Banking connections.

Best for: Privacy-conscious users, tracking total net worth, and those who want to connect with FCA-regulated advisers.

Consideration: Requires a slightly more proactive approach if you choose manual uploads over automated bank feeds.

3. The Privacy-First Approach to Budgeting

Many UK consumers are understandably wary of Open Banking. Giving an app read-only access to your bank account is secure, but it still involves sharing highly sensitive data with third-party servers.

If you value your privacy, a platform like Plouta offers a robust alternative. By using the Bank Statement Upload feature, you maintain total control over your data. You simply upload your monthly PDF or CSV statement, and the app categorises your spending retroactively. Coupling this with the Receipt Scanner gives you an itemised breakdown of your spending (e.g., separating grocery costs from alcohol on a supermarket receipt) without ever linking to your bank.

Expert Tip:If you are self-employed or run a side hustle, using a receipt scanner is vital. Capturing itemised receipts digitally ensures you don't miss allowable expenses when completing your self-assessment tax return for HMRC.

4. Moving Beyond Budgeting to Wealth Building

An expense tracker only tells you what you have spent. True financial wellbeing requires you to look at your entire wealth profile.

Once you have your monthly budget under control, you should be funnelling your surplus cash into tax-efficient wrappers like a Stocks and Shares ISA or your Workplace Pension. Using a Net Worth Tracker allows you to see the big picture: your property equity, your cash savings, your investments, and your pension pots, minus your outstanding mortgage and debts.

Common Mistakes to Avoid

Tracking Without Action: Logging your expenses is pointless if you do not adjust your behaviour. If you see you are overspending on dining out, you must lower the budget for the following month.

Ignoring Cash Flow Timing: A spreadsheet won't warn you if your bills go out before payday. Budgeting tools help you visualise your cash flow so you don't dip into an overdraft.

Forgetting Annual Expenses: People often budget perfectly for groceries but forget annual car insurance, MOTs, or Christmas. Divide these annual costs by 12 and save for them monthly.

Next Steps:

Managing your household finances shouldn't feel like a second job. By moving away from outdated spreadsheets and embracing modern digital tools, you can gain total control over your cash flow, eliminate wasteful spending, and start building meaningful wealth.

If you're looking for a simple way to track spending, monitor investments, understand your net worth, and improve your financial wellbeing with a privacy-first approach, Plouta provides the tools and expert support to help you stay on track.

Take the first step today: upload your bank statement, check your wellness score, and take back control of your financial future.

Your 30-Day Action Plan for Financial Control

Week 1: Assess and Audit

Download your chosen expense tracking app (like Plouta).

Check your Financial Wellness Score to understand your baseline.

Upload your last month's bank statement to see exactly where your money went.

Week 2: Clean Up and Categorise

Identify your core fixed expenses (mortgage, council tax, energy).

Spot the "leaks" — cancel at least two unused subscriptions or memberships.

Set a realistic limit for your "wants" category for the upcoming month.

Week 3: Build the Habit

Start using the Receipt Scanner immediately after making purchases to capture granular spending data.

Set up a direct debit to automatically move 20% of your income into an ISA or savings account on payday.

Week 4: Look to the Future

Input your property value, outstanding mortgage, and pension pots into your Net Worth Tracker.

Upload vital documents (insurance policies, Wills) to your secure Digital Vault.

If your net worth tracking reveals a shortfall for retirement, use the Adviser Matching feature to consult an FCA-regulated professional.

FAQs About Plouta Expense Tracker Feature

1. What is a Financial Wellness Score?

A Financial Wellness Score is a quick diagnostic metric that evaluates your overall financial health. It looks at your budgeting habits, debt levels, emergency savings, and long-term planning to highlight areas where you need to improve.

2. Why should I use a receipt scanner instead of just checking my bank feed?

A bank feed only shows the total amount spent at a merchant (e.g., £100 at Tesco). A receipt scanner breaks that down into itemised categories (groceries, alcohol, clothing), giving you much deeper insights into your actual consumption habits.

3. Does Plouta offer financial advice?

Plouta is a financial wellness technology platform and does not give regulated advice directly. However, the app features an Adviser Matching service that connects you with carefully vetted, FCA-regulated financial advisers for bespoke guidance.

4. How does manual bank statement upload work?

Instead of giving an app live access to your bank via Open Banking, you download your monthly statement as a PDF or CSV file from your online banking portal and upload it securely into the app. The app's AI then categorises the transactions for you.

5. What is the benefit of a Net Worth Tracker?

A Net Worth Tracker shifts your focus from short-term spending to long-term wealth building. By aggregating your assets (pensions, ISAs, property) and subtracting your liabilities, you can accurately track your progress toward financial freedom.

6. Is it safe to store my financial documents in an app?

Top-tier platforms utilize bank-level encryption. For example, storing your Will, insurance details, and pension records in a secure Digital Vault ensures they are safe from physical damage (like fire or flood) and accessible when you need them.

7. Can I track multiple bank accounts?

Yes. By uploading statements from different banks and credit cards, you can consolidate all your household finances into one unified wealth dashboard.

8. Does an expense tracker help with UK inflation?

Indirectly, yes. By tracking and reducing unnecessary expenses, you free up cash. If you invest that surplus cash into tax-efficient vehicles like a Stocks and Shares ISA, you give your money a chance to grow at a rate that outpaces inflation.

9. Can I share my budget with my spouse?

Yes. By using Family Finance Management tools, couples can review their combined cash flow, track shared goals, and stay accountable to their household budget without sharing individual bank logins.

10. What is the difference between an ISA and a Workplace Pension?

A Workplace Pension offers upfront tax relief and employer contributions but is locked until age 55 (rising to 57 in 2028). An ISA offers no upfront tax relief, but all growth and withdrawals are 100% tax-free, and you can access the money at any time.

Take control of your retirement, starting today.

Use Plouta to track your savings, forecast your retirement and get clear, practical advice tailored to your goals.

Disclaimer: Plouta is a financial wellness platform and does not provide regulated advice directly. All bespoke planning and professional recommendations are provided by our carefully selected, FCA-regulated partnered advisers. Tax treatment depends on your individual circumstances and legislation may change. Your capital is at risk.