How Plouta and Dedicated Advisers Unify Financial and Estate Planning

The Future of Your Legacy

Historically, financial planning and estate planning have been treated as two entirely separate worlds. You would manage your daily savings and investments on an app, check your pension statement once a year, and leave your Will in a physical paper file at a local solicitor’s office.

In 2026, this fragmented approach has become a serious threat to your family's wealth. With the standard Inheritance Tax (IHT) nil-rate band frozen at £325,000 until 2031 and a major overhaul set for April 2027 that brings unused pension pots into the scope of IHT for the first time, wealth preservation now requires a unified strategy.

Achieving true financial peace of mind requires a system that bridges the gap between everyday digital wealth tracking and expert, regulated legal advice. This guide explains how the Plouta app and our network of vetted, professional advisers work together to secure your financial future and protect your family's legacy.

How do Plouta and dedicated advisers help with financial and estate planning?

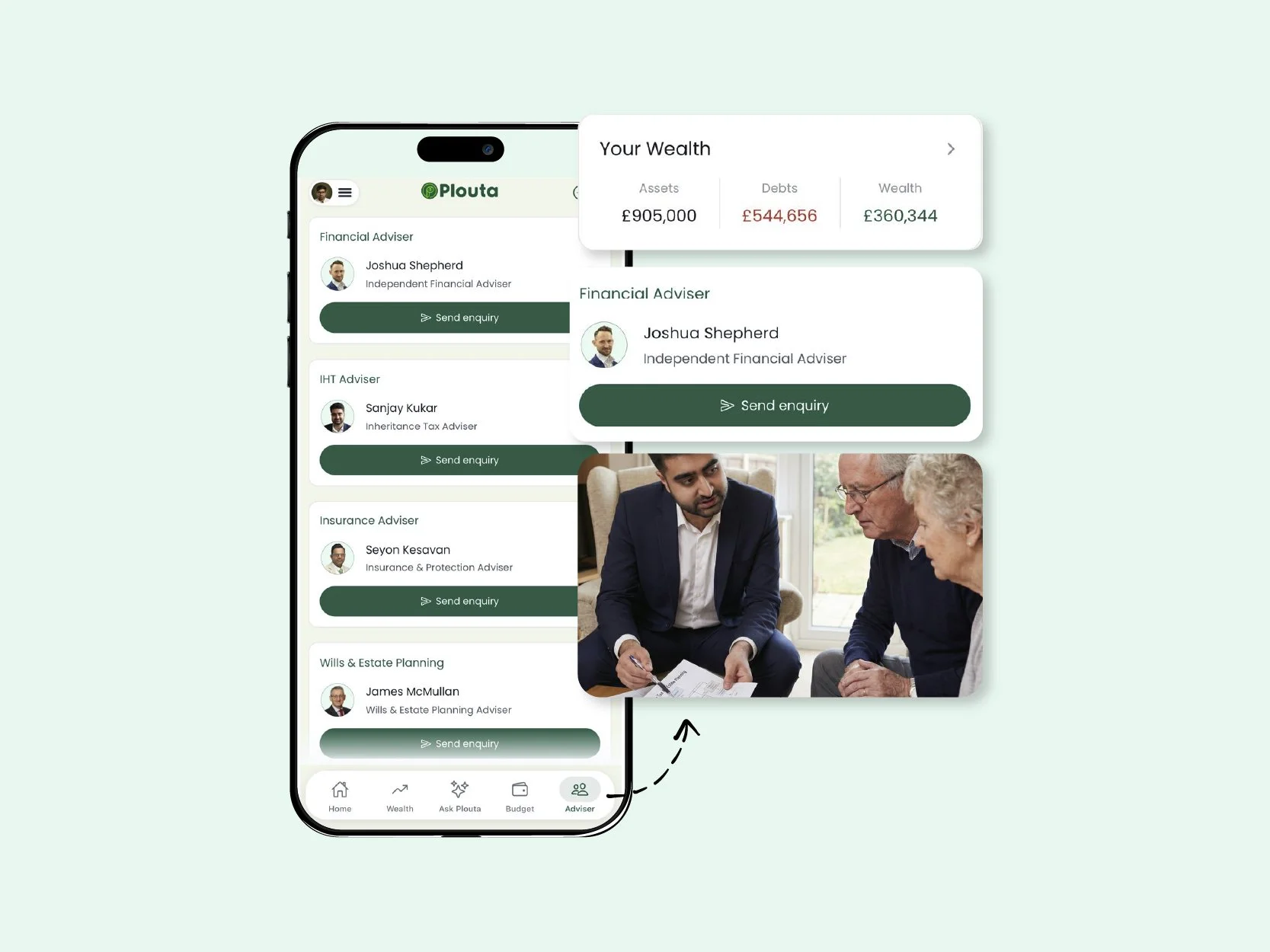

Plouta provides the digital foundation by letting you track your live Net Worth, run diagnostic checks with a Financial Wellness Score, and securely store estate-critical documents (like Wills, pension statements, and trust deeds) inside an encrypted Digital Vault. When complex tax laws, pension rules, or estate structures require professional action, Plouta’s Adviser Matching service connects you directly with vetted, FCA-regulated financial advisers and SRA-regulated solicitors. Together, they build a watertight, tax-efficient roadmap that ensures your wealth is optimized during your lifetime and passed on to your loved ones exactly as you intend.

1. The Shifting UK Landscape: Why Legacy Planning is More Urgent in 2026

Estate planning is no longer a task reserved only for the ultra-wealthy. Rising property values, coupled with frozen tax thresholds, have pulled thousands of middle-income UK families into the IHT net.

The April 2027 Pension Tax Change

Currently, most private and workplace pensions sit outside your estate for IHT purposes. However, from 6 April 2027, the residual value of defined contribution pensions will be treated as part of your taxable estate upon death. This reform is projected to bring an additional 10,500 estates a year into the IHT bracket and significantly increase the tax bills of 38,500 more.

The Frozen Thresholds

Nil-Rate Band (NRB): Frozen at £325,000 per person until April 2031.

Residence Nil-Rate Band (RNRB): Frozen at £175,000 per person when leaving a main residence to direct descendants.

The Taper Threshold: The RNRB reduces by £1 for every £2 your estate exceeds £2 million. The inclusion of pensions from 2027 means many more families will cross this £2 million line, accidentally wiping out their home allowances.

Step 1: Digital Clarity (How the Plouta App Organises Your Wealth)

Before you can construct a legally binding estate plan, you must understand your current financial baseline. Plouta acts as your digital financial "life book," replacing scattered spreadsheets with unified, real-time tracking.

The Net Worth Tracker & Wealth Dashboard

To calculate potential IHT liabilities, you must aggregate your property values, cash savings, investment portfolios, and pension pots, and then subtract your mortgage and any debts. Plouta's Net Worth Tracker does this automatically, keeping your total net position live and visible.

The Financial Wellness Score

How tax-efficient are your investments? Have you maximized your £20,000 ISA allowance? Is your life insurance wrapped in a trust so it pays out fast and free of tax? Plouta's instant Financial Wellness Score audits your current holdings, highlighting critical estate planning blindspots within minutes.

The Secure Digital Vault

A major point of friction during probate is locating physical paperwork. Executors often spend months hunting down old pension reference numbers, paper Wills, and policy terms. Plouta's Digital Vault provides an encrypted, secure depository where you can store:

Up-to-date Wills and Letter of Wishes.

Trust Deeds and Lasting Powers of Attorney (LPA).

Pension statement summaries and life insurance documents.

This ensures your executors have immediate, authenticated access to your "life folder" when it is needed most.

Step 2: Professional Execution (How Dedicated Advisers Secure Your Legacy)

While a digital app is highly effective for tracking and organization, it cannot draft a legally binding Will or restructure a multi-million-pound pension pot. That is where the power of dual-regulated human expertise comes in.

Through Plouta’s Adviser Matching service, you are seamlessly connected to vetted, independent professionals:

FCA-Regulated Financial Advisers

A financial adviser manages your wealth during your lifetime to minimize tax:

Pension Restructuring: Preparing your pension drawdown strategy for the 2027 rules, ensuring you draw down funds in the most tax-efficient order.

Gifting Strategies: Utilizing Potentially Exempt Transfers (PETs), such as the seven-year rule, and regular gifts out of normal surplus income to safely reduce your taxable estate.

IHT Mitigation: Recommending specialised tax-planning vehicles, such as Discounted Gift Trusts or Business Relief qualifying investments, where appropriate.

SRA-Regulated Solicitors

An estate planning solicitor handles the legal mechanics of your legacy:

Writing and Updating Wills: Ensuring your Will is legally binding and reflects modern tax allowances.

Setting Up Trusts: Creating discretionary, bare, or bypass trusts to control exactly how and when your beneficiaries receive their inheritance.

Lasting Power of Attorney (LPA): Establishing health and financial LPAs so a trusted person can manage your affairs if you lose mental capacity.

Real-Life Example: Preparing for the 2027 Pension IHT Shift

The Problem: David (57) and Helen (55) had a combined estate worth £1.4 million, which included their family home, ISAs, and cash. Because their estate sat below the combined £1 million married allowance and they had £600,000 in defined contribution pensions (which they believed were exempt from IHT), they felt their estate plan was complete.

The Catch: With the 2027 rule changes, their taxable estate would rise from £1.4 million to £2 million once David's pensions were factored in. This would immediately trigger a 40% IHT bill of £400,000 on everything over their £1 million allowance, plus threaten to taper away their Residence Nil-Rate Band.

The Action: David used the Plouta app to aggregate his assets, highlighting the massive tax leak on his Financial Wellness Score. Through Plouta, he connected with an FCA-regulated financial adviser and an SRA-regulated estate solicitor.

The Solution: The adviser constructed a drawdown plan to gradually spend down the pension assets first while keeping their tax-free ISAs growing. The solicitor drafted a discretionary trust structure to gift surplus lifetime income to their children.

The Result: They successfully reduced their projected IHT exposure, protected their children's inheritance, and gained absolute peace of mind.

Common Mistakes to Avoid

Waiting Too Long to Maximize Cash Allowances: The window to put £20,000 entirely into a Cash ISA closes in April 2027. Missing the current 2026/27 tax year allowance means losing that tax-free cash capacity forever.

Leaving Idle Cash in a Brokerage Account: From 2027, holding uninvested cash in a Stocks and Shares ISA will trigger a 22% tax on the interest. Always ensure your funds are actively invested.

Ignoring UK Inflation: Relying purely on cash or instruments like Premium Bonds rarely outpaces UK Inflation over the long term. Failing to invest is the biggest risk to your long-term purchasing power.

The Value of Tax-Efficient Savings (Statistics)

The Investment Gap: The government reduced the Cash ISA limit because billions of pounds are sitting in low-yield cash accounts. Historically, global equities have returned an average of 7-9% annually, significantly outperforming cash over 10-year periods.

Tax Threshold Freezes: With income tax thresholds frozen until 2031, "fiscal drag" is pulling more workers into higher tax bands. Sheltering your money from tax is more urgent than ever.

Savings Tax Hike: From April 2027, the basic rate of tax on savings interest outside of an ISA will jump to 22%, making the tax-free ISA wrapper incredibly valuable.

The UK savings landscape is undergoing its biggest transformation in a decade. While the upcoming reduction of the Cash ISA limit to £12,000 may seem daunting, it serves as a crucial nudge to start investing for long-term growth. By understanding the anti-circumvention rules like the 22% tax on uninvested cash and new transfer restrictions you can shield your wealth from unnecessary penalties.

If you're looking for a simple way to track spending, monitor investments, understand your net worth and improve your financial wellbeing, Plouta provides the tools and expert support to help you stay on track. Don't wait until 2027 to adjust your strategy; use your allowances wisely today and secure your financial freedom.

Frequently Asked Questions

Do pensions pay Inheritance Tax in the UK?

Currently, defined contribution and defined benefit pensions do not form part of your taxable estate on death and are exempt from IHT. However, from 6 April 2027, unused pension pots and pension death benefits will be included in your estate valuation and taxed at up to 40%.

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting framework where 50% of your take-home pay is allocated to essential needs (mortgage, groceries), 30% to wants (discretionary spending), and 20% to savings, investments, and long-term financial planning.

How does the seven-year rule work for gifts?

Any cash or asset you gift to an individual during your lifetime is classified as a Potentially Exempt Transfer (PET). If you survive for seven years after making the gift, it falls completely outside your estate for IHT purposes. If you die within seven years, it is brought back into your estate, though the tax rate may taper down after year three.

What is a Residence Nil-Rate Band (RNRB)?

The RNRB is an additional IHT allowance of £175,000 per person available when you leave your main family home to your direct descendants (children or grandchildren). It is frozen until April 2031 and tapers away for estates worth over £2 million.

Why do I need both a financial adviser and a solicitor?

A financial adviser manages your asset growth, pension drawdowns, and tax efficiency while you are alive. An SRA-regulated solicitor handles the legal execution of your estate, such as writing Wills, setting up trusts, and managing the probate process. Using both ensures your estate plan is both financially optimized and legally airtight.

What is the difference between an executor and a beneficiary?

An executor is the person legally responsible for administering your estate, paying off any debts, and distributing your wealth after you die. A beneficiary is an individual or organization named in your Will who receives a portion of your estate.

How does the Nil-Rate Band transfer work?

If a spouse or civil partner passes away and leaves their entire estate to the survivor, their unused £325,000 nil-rate band transfers to the survivor. This allows the surviving partner to potentially pass on up to £650,000 (or £1 million with the home allowance) tax-free on their death.

Does cohabiting with a partner offer the same tax exemptions as marriage?

No. Cohabiting couples do not benefit from the spousal exemption. Anything left to a cohabiting partner is subject to standard IHT rules once the value exceeds the individual £325,000 nil-rate band.

Are life insurance payouts subject to Inheritance Tax?

If a life insurance policy is paid directly to your estate, it will be included in your IHT calculations. However, if the policy is written "in trust" (an easy legal wrapper your adviser can implement), the payout goes directly to your beneficiaries tax-free and without waiting for probate.

What is a Lasting Power of Attorney (LPA)?

An LPA is a legal document that allows you to appoint one or more trusted people (your attorneys) to make decisions on your behalf if you suffer a sudden medical emergency or loss of mental capacity.

Can I change my Will after it has been signed?

Yes. You can make minor alterations by adding a legal document called a "codicil." For major changes, it is highly recommended to have an SRA-regulated solicitor draft an entirely new Will to prevent legal disputes.

What is probate, and why does it take so long?

Probate is the legal process of proving that a Will is valid, valuing the deceased's assets, paying any outstanding tax, and distributing the inheritance. It is often delayed by lost paperwork, which is why utilizing a secure digital vault is crucial.

Can I give regular gifts out of my income tax-free?

Yes. Gifts made out of regular, surplus income are immediately exempt from IHT. However, the gifts must not reduce your standard of living, and you must maintain detailed records of your income and expenditure to prove the surplus.

Are business assets exempt from Inheritance Tax?

Through Business Property Relief (BPR), qualifying family businesses and agricultural assets can pass with up to 100% IHT relief. However, changes taking effect in April 2026 will cap the 100% relief at £1 million, with anything above that taxed at an effective rate of 20%.

How secure is Plouta's Digital Vault?

Plouta uses advanced, bank-grade encryption to protect your sensitive financial and estate documents. Access permissions are strictly isolated at the database level, ensuring your information remains private until you explicitly grant access to your executors or advisers.

Your 30-Day Legacy Action Plan

Week 1: Document & Audit

Download the Plouta app and check your Financial Wellness Score.

Link your active assets to calculate your live, aggregate Net Worth.

Search for any "lost" pensions from previous employers and record their details.

Week 2: Build the Vault

Locate your physical Will, Lasting Power of Attorney, and major insurance policies.

Scan and upload these documents to your secure, encrypted Digital Vault.

Draft a simple Letter of Wishes outlining who should inherit sentimental items.

Week 3: Model the IHT Risk

Estimate the total value of your estate, including your family home and all private pension pots.

Calculate if your total wealth (including pensions) is likely to exceed your combined married or single Nil-Rate Bands.

Week 4: Secure Regulated Advice

Use Plouta’s Adviser Matching feature to connect with an FCA-regulated planner or SRA-regulated solicitor.

Present your Digital Vault records to your matched professional to construct a tailored plan to mitigate the upcoming 2027 tax changes.

Financial tracking gives you the control to build wealth, but estate planning gives you the power to protect it. By combining elegant digital management with the uncompromised wisdom of FCA and SRA-regulated professional advice, you secure your family's future and preserve your hard-earned legacy.

If you're looking for a simple way to track spending, monitor investments, understand your net worth, secure your estate documents, and access expert advice, Plouta provides the unified tools and professional support to help you stay on track.

Take control today: calculate your net worth, secure your documents, and connect with a Plouta-vetted adviser to future-proof your legacy.

Take control of your retirement, starting today.

Use Plouta to track your savings, forecast your retirement and get clear, practical advice tailored to your goals.

Disclaimer: Plouta is a financial wellness platform and does not provide regulated advice directly. All bespoke planning and professional recommendations are provided by our carefully selected, FCA-regulated partnered advisers. Tax treatment depends on your individual circumstances and legislation may change. Your capital is at risk.